Offset Loan Accounts Explained

An offset account is truly a powerful tool if used correctly. Offset accounts are used by both home and investment loan borrowers as a great tool to save interest on your home and paying off your home sooner, as well as tax planning for investors.

How do offset accounts work?

They can be called: offset account, interest offset account, mortgage offset account or offset home loan. They are all interchangeable terms and describe a separate account which is linked to a loan and offsets the interest charged to that loan.

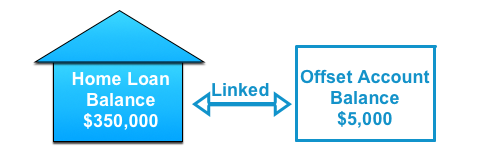

For example: say you owed $350,000 on your home loan today and had $5000 in your offset account. The lender calculates the interest on your home based on the amount owing on the loan less any offset balance. See below – the interest calculated would be based on a net balance of $345,000 rather than $350,000. This saves you interest over the month.

Let’s imagine, that you owed $350,000 on your loan and you had $350,000 sitting in your offset account (this would be nice wouldn’t it!). In this case you would not be charged interest at all.

How is interest calculated using an offset account?

Interest on a home or investment loan is usually calculated daily, so, based on the daily balance of your offset account you can calculate the interest saving that the offset account will give you. To do the calculation you will need to know the interest rate that you are paying on your loan.

For Example; say your interest rate is 5% pa and you expect the average balance of the offset account to be around $10,000 per day. Then you would potentially save $500 on your home loan interest. $10,000 × 5.00% pa = $500 pa savings

You can play with your own figures using the offset calculator at:

http://www.ifca.net.au/loan-calculators/home-loan-offset-calculator/

Should you use an offset?

The above example demonstrates a significant saving on your annual interest, which is relevant to the amount of money sitting in your offset account each day. An offset account is not going to have much impact / produce much interest savings if there are limited funds in the offset account. Before deciding that you need an offset account, firstly find out if there are any extra fees or perhaps a higher interest rate for the use of an offset account. There are some lenders that provide offset accounts for lower fees with no rate change, however some lenders only offer offset accounts as part of a package which can cost up to $400 per year.

Sometimes it could still be beneficial to take a more expensive loan with an offset account incurring an annual fee, if the offset account is being used for tax planning purposes.

An offset account is a deposit product and does need a licensed financial advisor to advise on suitability for your situation, however, below are some general advantages of offset accounts for this purpose. Please seek qualified financial advice of your situation.

Is an offset affected by how I pay my loan?

Money in your offset account will always offset the interest you would have paid on your loan, however the minimum repayments will be affected by the type of loan repayments you have.

a) Principle & interest loans

If you pay principle and interest loan repayments, your repayments won’t change regardless of how much cash you have in your offset account. In this case, more of your repayment will go to the principle of your loan, so you will effectively be paying off your loan faster. For example, say you had the $350,000 loan as above and you had $100,000 in your offset account, you would be paying interest on only $250,000 however repayments would be based on $350,000. That means more of your regular fortnightly or monthly repayments would be going to pay off your loan.

b) Interest only repayments.

If your loan has true interest only repayments then the monthly repayments on your loan will be something like this: (The loan balance – Offset account balance) × current % ÷ 12 = monthly repayments

c) Interest based repayments

A few lenders have interest based loans whereby the minimum repayments are set at whatever the monthly interest repayment would on the loan be assuming there was no offset account balance. For these types of loans the offset account still offsets your interest but repayments will remain constant. In effect these loans act more like principle and interest loans but with lower minimum repayment required as any offset benefit will be paid off the principle of your loan.

Is it better to pay funds into the loan or use an offset account?

The calculation stats that paying funds into your loan has the same effect as if those same funds were sitting in your offset account. For example, if you decided to pay $5,000 into your loan rather than leaving it in your separate offset account the interest for the day would still be calculated based on $345,000, there is no difference to the calculation as the interest calculation for that particular day is the same. The difference is that the funds are either redrawn if in the loan or sitting in a transaction offset account.

Tax deductibility of loan redraw versus funds in an offset account

There is one fundamental difference between redraw and offset accounts and that is funds paid into a loan and then redrawn for non investment purposes will affect the tax deductibility of the loans interest going forward where as funds paid into an offset account and subsequently used (for whatever purpose) do not affect the loans potential for tax deductions going forward.

If the loan is an investment loan or if the intention is to convert it to an investment loan in the future then paying funds into a loan then using redraw for personal purposes is a mistake that can’t be undone.

For example: If you had a home loan of $700,000 and paid $200,000 into the loan reducing the amount to $500,000, then decided to redraw $200,000 for non investment purposes, your loan balance would again be $700,000 and the interest on the loan would be calculated as such.

However, if you decided to change the property to an investment, and redraw the $200,000, this would not be tax deductible as the funds were used for non investment purposes. Effectively meaning you could only claim an interest deduction on part of the loans balance ($500,000) going forward.

If the $200,000 were placed in an offset account then potentially the interest on the full loan balance of $700,000 could be claimed going forward. It is only a slight difference, but very significant and could cost you thousands of dollars in lost deductions over many years.

As another example, say the $200,000 was redrawn instead of placing the funds in the offset account. $200,000 x 6% pa = $12,000 pa in lost interest deductions each year. If you have the property / loan for 15 years then this would potentially equate to losing $180,000 in tax deductions over that time! Worth thinking about!

What are the benefits of turning your home loan into an investment loan and maximising future tax deductibility

This is a common scenario, where paying down the home loan is not such a good idea. Commonly, people buy a home, then a few years later after paying down their loan, property price increasing and gaining equity and increased incomes, they are in a position to upgrade. People want to retain their existing home and rent it out as an investment property. As they have paid the home loan down they now end up with a small investment property loan and usually a much bigger owner occupied loan. From a tax point of view it is almost always better the other way around!

The offset account can help with this situation with a bit of planning.

You can set up the home loan with an offset account and rather than paying off the loan with extra repayments, these payments go into the offset account. The interest is exactly the same, however over time you would hopefully have a large pile of money in your offset account and importantly the loan balance will still maximise the interest deductibility going forward.

When the time is right to purchase again, you simply draw the money from the offset account and use this as all or part of your deposit on the new purchase and the existing loans interest would become tax deductible with a higher loan balance than if you had paid excess funds into the loan.

Remember that redrawing funds from any loan would be considered a new loan in the eyes of the tax man and the purpose of the redrawn funds would determine if the interest on the redrawn funds was tax deductible or not.

An interest only loan would be the optimal set up as the balance of the loan would not decrease over time which would in turn mean you could maximise the potential benefits of this strategy. Most lenders allow up to 10 years of a loan term to be interest only.

Even with a reducing loan balance with principal and interest repayments this strategy would still be much more effective than if excess funds had been paid into the loan itself provided only the minimum repayments are made.

Summary

An offset account can be a really great loan feature. With a little planning investors and general home owners can use an offset account to their benefit and maximise their future tax deductibility benefits.

An offset account linked to an interest only loan is perhaps the most flexible of all loan set ups as it allows for any eventuality.

If you would like to know more about how an offset account could work for you contact us on our express enquiry form.